Research@Ourso: A Perfect Storm

May 26, 2026

Louisiana is no stranger to natural disasters, but a perfect storm of circumstances may be making it harder to own a home in a new way.

As severe weather events increase in frequency and strength, homeowners insurance is not just getting more expensive; in many areas, insurance options are disappearing altogether. Junior Betanco Gunera, a PhD student in the LSU Department of Finance, examined how this insurance crisis is reshaping how banks approach mortgage lending, with potential implications for homeownership.

Betanco Gunera recently presented a preliminary version of his research at both the 2026 Eastern Finance Association (EFA) and the 2025 Financial Management Association (FMA) annual meetings. His study utilized a groundbreaking dataset from a 2024 U.S. Senate Budget Committee investigation, which examined approximately 249 million insurance policies across all 50 states and the District of Columbia from 2018 to 2023. Additionally, it incorporated loan records from the Home Mortgage Disclosure Act (HMDA).

Fast Facts

When insurers chose not to renew policies in high-risk areas, as measured by the Non-Renewal Rate (NRR), banks responded. Each 1% increase in NRR led to measurable lending impacts the following year.

Fewer Approvals...

A ~0.392 percentage point decrease in mortgage approval rates.

...Similar Costs

Mortgage size and interest rates remained mostly unchanged.

Impacts

The findings suggest that the real danger of a weakening insurance market may not necessarily be a total collapse of lending, but instead a shift towards more restrictive lending standards.

Instead of making mortgages more expensive through higher interest rates, the data showed that in counties with stressed (high NRR) insurance markets, banks had lower loan approval rates, suggesting a rise in outright rejections rather than higher borrowing costs. This form of tightened lending has significant impacts for consumers and policymakers alike.

Threats to Equity

Under normal conditions, homeowners' insurance protects homeowner equity and serves as collateral protection for lenders. However, if a home becomes harder to insure through the private market or is pushed into an expensive government-run “last resort” market, its resale value may be limited. This is because potential buyers may have a harder time obtaining mortgage approval, which can chill the property market and diminish the equity that homeowners have spent years building.

Regulatory Challenges

Typical indicators, such as average interest rates or total lending volumes, did not capture the shift in lender behavior, potentially creating blind spots for policymakers and regulators. Betanco Gunera suggests that greater coordination is needed among insurance regulation, housing policy, and financial regulators to monitor how the health of the insurance market is impacting credit access.

PhD Student, LSU Department of Finance

Which communities are most affected?

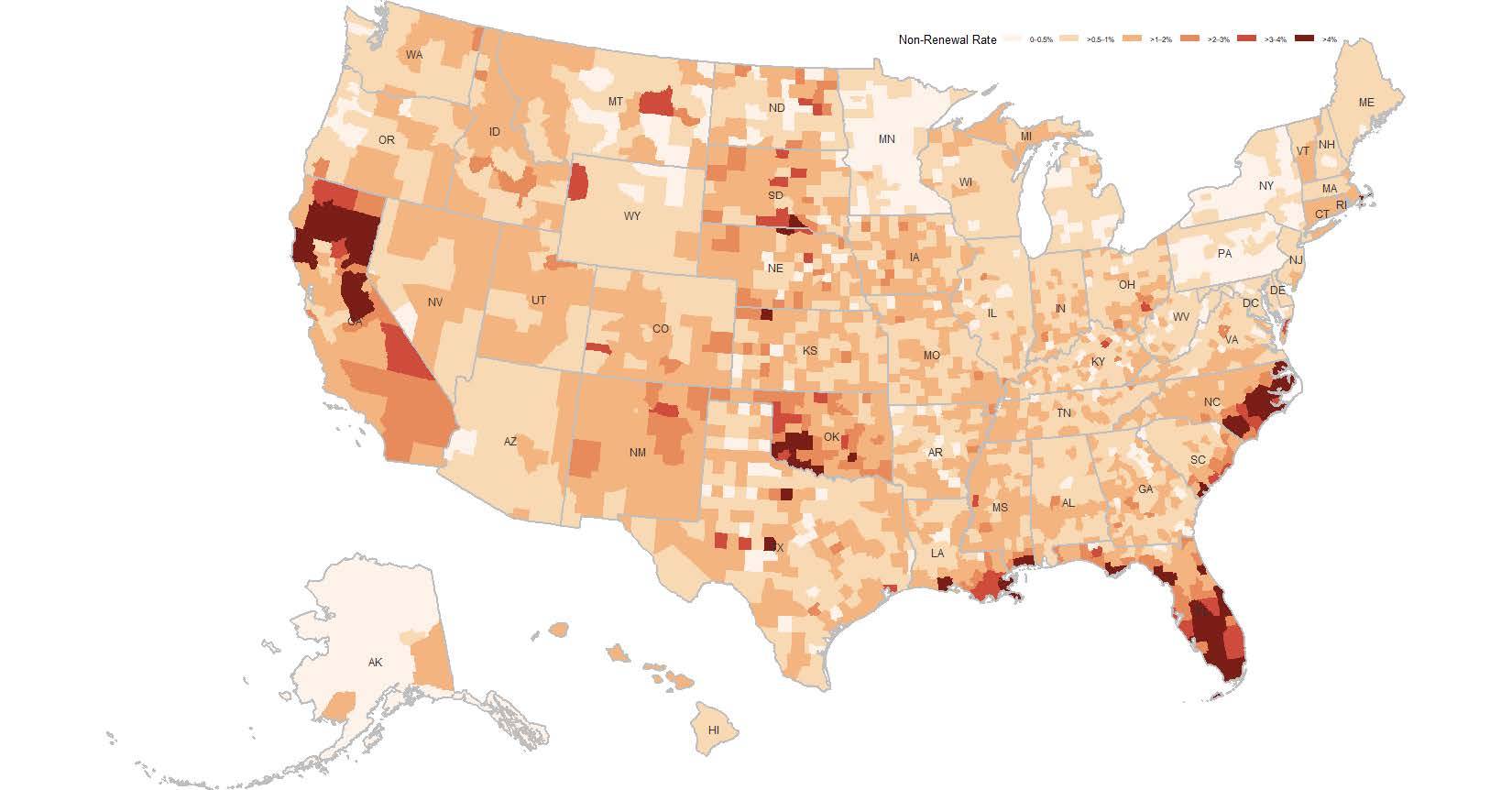

The 2024 congressional dataset allowed Betanco Gunera to map homeowner insurance non-renewal rates (NRR) by county across the United States. In the map below, darker shades of red represent higher (worse) NRR, with significant concentrations appearing along the coastlines of Louisiana, Florida, and North Carolina, as well as throughout central and northern California. Lighter shades indicate lower (better) NRR across the Midwest and Northeast.